High balance transfer credit cards offer a potential lifeline for those burdened by high-interest debt. These cards, specifically designed to help individuals consolidate and manage their existing balances, often come with enticing introductory APRs, making them a tempting option for debt relief. But before diving headfirst into a balance transfer, it’s crucial to understand the intricacies of these cards, including their eligibility requirements, interest rates, fees, and potential pitfalls.

The allure of a low introductory APR can be deceptive, as these rates are usually temporary, often lasting only a few months. Once the promotional period ends, the APR typically reverts to a standard rate, which can be significantly higher. This shift can leave you with a substantial debt burden if you’re unable to pay off the balance before the introductory period expires. Moreover, balance transfer fees, often a percentage of the transferred amount, can add to your overall debt.

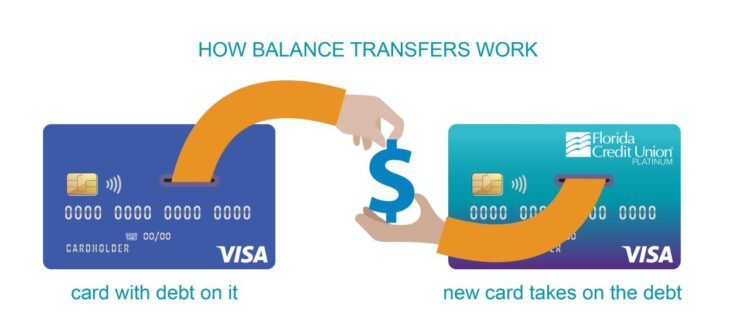

What are High Balance Transfer Credit Cards?

High balance transfer credit cards are a type of credit card specifically designed to help individuals consolidate high-interest debt from other credit cards into a single account with a lower interest rate. This allows cardholders to save money on interest charges and potentially pay off their debt faster.

These cards are often marketed to consumers with significant credit card debt, offering a temporary promotional period with a low introductory APR (Annual Percentage Rate) for balance transfers. This period typically lasts for a set timeframe, after which the APR reverts to a higher standard rate.

Typical Features of High Balance Transfer Cards

These cards are designed to assist consumers in managing their debt effectively. Here are some common features:

- Balance Transfer Introductory APR: The most prominent feature is a low introductory APR offered for a limited time, usually 0% or a very low percentage. This helps borrowers save significantly on interest charges during the promotional period.

- Balance Transfer Fee: A fee is often charged for transferring balances from other credit cards. The fee percentage varies depending on the issuer and can range from 3% to 5% of the transferred amount.

- Minimum Payment Requirements: These cards typically have minimum monthly payment requirements, but the exact amount depends on the issuer and the outstanding balance.

- Credit Limit: The credit limit on a high balance transfer card is determined by the issuer based on the applicant’s creditworthiness.

- Rewards Program: Some high balance transfer cards offer rewards programs, such as cash back or travel miles, to incentivize cardholders.

Benefits of Using High Balance Transfer Cards

High balance transfer cards offer several potential benefits for individuals seeking to manage their debt:

- Lower Interest Rates: The introductory APR on these cards is significantly lower than the standard APR on many other credit cards. This allows borrowers to save money on interest charges and potentially pay off their debt faster.

- Debt Consolidation: These cards help consolidate multiple high-interest debts into a single account with a lower interest rate. This simplifies debt management and reduces the risk of missed payments.

- Flexible Payment Options: Many high balance transfer cards offer flexible payment options, such as online payment portals and mobile apps, allowing cardholders to manage their accounts conveniently.

Eligibility and Requirements

To be eligible for a high balance transfer credit card, you’ll need to meet certain criteria, which vary depending on the issuer. However, some common factors play a crucial role in determining your approval.

Credit Score Requirements

Credit score is a significant factor in determining your eligibility for a high balance transfer card. Lenders typically prefer applicants with good to excellent credit scores, as it indicates a history of responsible financial behavior.

A credit score of at least 700 is generally considered good, while a score of 740 or higher is excellent.

Income and Debt-to-Income Ratio

Lenders also consider your income and debt-to-income (DTI) ratio. A higher income can indicate your ability to manage the transferred balance, while a lower DTI ratio shows that you have sufficient disposable income to make payments.

Your DTI ratio is calculated by dividing your monthly debt payments by your gross monthly income. A DTI ratio below 36% is generally considered favorable.

Documentation Needed for Application

When applying for a high balance transfer credit card, you’ll typically need to provide the following documentation:

- Personal information: This includes your full name, address, Social Security number, and date of birth.

- Employment information: This may include your employer’s name, address, and phone number, as well as your annual income.

- Financial information: This may include your bank account information, credit card statements, and other debt information.

Interest Rates and Fees

High balance transfer credit cards often come with enticing introductory offers, but understanding the interest rates and fees associated with them is crucial to making an informed decision. This section will explore the nuances of these financial aspects and how they can affect your overall cost.

Introductory APRs and Standard APRs

Introductory APRs are temporary rates offered for a specific period, typically 0% or a low percentage, to entice you to transfer a balance from another card. These promotional periods can range from 6 to 18 months. However, after the introductory period expires, the standard APR kicks in, which is usually much higher.

Fees Associated with Balance Transfers

Balance transfer cards may charge fees for transferring your balance. Common fees include:

- Transfer Fees: These are typically a percentage of the amount transferred, usually ranging from 1% to 5%. For example, a 3% transfer fee on a $10,000 balance would cost you $300.

- Annual Fees: Some cards charge an annual fee, which can range from $0 to $100 or more. It’s important to factor in these fees when comparing cards.

Impact of Rates and Fees on Overall Costs

The interest rates and fees associated with balance transfer cards can significantly impact your overall cost. Here’s how:

Example: You transfer a $10,000 balance to a card with a 0% introductory APR for 12 months and a 20% standard APR. After the introductory period, you haven’t paid off the entire balance. You’ll start accruing interest at the 20% standard APR. If you only make minimum payments, the interest charges can quickly add up, making it difficult to pay off the balance.

- Interest Accrual: Even with a 0% introductory APR, interest continues to accrue during the promotional period. This interest is often capitalized, meaning it’s added to your balance at the end of the introductory period. This can lead to a larger balance than the original amount you transferred.

- Fees Impact: Transfer fees and annual fees can significantly increase the overall cost of transferring your balance.

Transfer Process and Timeline

Transferring a balance to a high balance transfer credit card is a straightforward process, but it’s essential to understand the steps involved and the typical timeline for approval and processing.

Here’s a step-by-step guide to the transfer process:

Applying for a Balance Transfer Card

The first step is to apply for a high balance transfer credit card that meets your needs. This involves providing personal and financial information, such as your Social Security number, income, and credit history. The issuer will then review your application and make a decision based on your creditworthiness.

Balance Transfer Request, High balance transfer credit card

Once your application is approved, you can initiate the balance transfer. This typically involves contacting the credit card issuer and providing the following information:

- The account number and balance you want to transfer

- The name of the creditor you are transferring the balance from

- The amount you want to transfer

Processing and Approval

After you submit your balance transfer request, the credit card issuer will process it. This typically involves verifying the information you provided and contacting your previous creditor to confirm the balance. Once the transfer is approved, the issuer will send the funds to your previous creditor.

Timeline for Balance Transfer Approvals and Processing

The timeline for balance transfer approvals and processing can vary depending on the credit card issuer and the complexity of the transfer. However, it typically takes 7 to 14 business days for the transfer to be completed. Here’s a possible timeline:

- Application Approval: 1-3 business days

- Balance Transfer Request Processing: 2-5 business days

- Funds Transfer to Previous Creditor: 2-7 business days

Managing the Transfer Process

Here are some tips for managing the balance transfer process:

- Apply early: Applying for a balance transfer card well in advance of your due date gives you ample time to complete the process.

- Check for fees: Be sure to review the terms and conditions of the balance transfer card carefully, including any fees associated with the transfer.

- Monitor your account: Keep track of your balance transfer request and ensure that the funds have been transferred successfully.

- Contact customer service: If you have any questions or concerns about the transfer process, contact the credit card issuer’s customer service department.

Potential Challenges or Delays

Here are some potential challenges or delays that might occur during the balance transfer process:

- Creditworthiness: If your credit score is not high enough, you may not be approved for a balance transfer card.

- Transfer limits: Some credit cards have limits on the amount you can transfer.

- Processing delays: There may be delays in processing the transfer due to issues with your previous creditor or the credit card issuer.

Comparison with Other Debt Consolidation Options: High Balance Transfer Credit Card

High balance transfer credit cards are a popular option for debt consolidation, but they are not the only choice. Other options, such as personal loans and debt consolidation loans, can also be effective. Each option has its own advantages and disadvantages, and the best choice for you will depend on your individual circumstances.

Comparison of Debt Consolidation Options

Here’s a comparison of high balance transfer credit cards, personal loans, and debt consolidation loans, highlighting their key features and suitability:

| Feature | High Balance Transfer Credit Card | Personal Loan | Debt Consolidation Loan |

|---|---|---|---|

| Interest Rates | Typically lower introductory rates, but can be higher after the introductory period | Fixed interest rates, usually higher than introductory rates on balance transfer cards | Fixed interest rates, usually higher than introductory rates on balance transfer cards |

| Fees | Balance transfer fees, annual fees, and potential late payment fees | Origination fees, prepayment penalties | Origination fees, prepayment penalties |

| Eligibility | Good credit score, sufficient income | Good credit score, sufficient income | Good credit score, sufficient income |

| Flexibility | Offers a 0% APR period for transferring balances, but may have a minimum payment | Fixed monthly payments, may offer flexibility in repayment terms | Fixed monthly payments, may offer flexibility in repayment terms |

| Suitability | Ideal for consolidating high-interest debt, especially if you can pay it off within the introductory period | Suitable for borrowers with good credit and a steady income, looking for a fixed payment structure | Similar to personal loans, but specifically designed for debt consolidation |

Suitability of Each Option Based on Individual Circumstances

- High balance transfer credit cards are suitable for individuals with good credit who need to consolidate high-interest debt. If you can pay off the balance within the introductory period, you can save significantly on interest charges. However, if you are unable to pay off the balance before the introductory period ends, you will be subject to the standard APR, which can be higher than the introductory rate.

- Personal loans are a good option for individuals with good credit who need a fixed monthly payment structure. They offer fixed interest rates, making it easier to budget and track your payments. However, personal loans typically have higher interest rates than balance transfer credit cards, so they may not be the best option if you are looking to save on interest charges.

- Debt consolidation loans are similar to personal loans but are specifically designed for debt consolidation. They can help you simplify your payments and reduce your monthly expenses. However, they may have higher interest rates than balance transfer credit cards, and they may not be as flexible as other options.

Strategies for Successful Use

A high balance transfer credit card can be a powerful tool for debt consolidation and saving money on interest, but it’s crucial to use it strategically to maximize its benefits. This involves planning for repayment, avoiding further debt accumulation, and managing your credit utilization effectively.

Creating a Repayment Plan and Sticking to It

Developing a realistic repayment plan is essential to ensure you pay off your transferred balance before the promotional period ends. This will help you avoid reverting to high interest rates.

- Determine Your Minimum Monthly Payment: Calculate the minimum payment required to avoid late fees and keep your account in good standing.

- Set a Higher Payment Goal: Aim to pay more than the minimum each month to accelerate your debt repayment. This can be done by allocating a portion of your budget or finding extra income sources.

- Consider Debt Snowball or Avalanche Method: The snowball method focuses on paying off the smallest debts first, providing quick wins and motivation. The avalanche method prioritizes debts with the highest interest rates, leading to greater long-term savings.

- Automate Payments: Set up automatic payments to ensure consistent and timely contributions towards your debt.

Avoiding Additional Debt Accumulation

It’s vital to resist the temptation to use your high balance transfer card for new purchases.

- Stick to a Budget: Create a detailed budget to track your income and expenses, and avoid overspending. This will help you stay on track with your repayment plan.

- Limit the Use of Other Credit Cards: Focus on paying down your existing debt before using other credit cards. This helps avoid accumulating further debt and interest charges.

- Avoid Cash Advances: Cash advances come with high interest rates and fees. Resist the urge to use your card for quick cash.

Managing Credit Utilization and Minimizing Interest Charges

Credit utilization is the percentage of available credit you are using. It plays a significant role in your credit score.

- Keep Credit Utilization Low: Aim for a credit utilization ratio of 30% or less. This indicates responsible credit management and can improve your credit score.

- Monitor Your Credit Score Regularly: Check your credit score periodically to ensure your utilization remains within a healthy range. You can access your credit score through various online services.

- Make Payments on Time: Late payments can negatively impact your credit score and increase interest charges. Set up reminders or automate payments to avoid missing deadlines.

Potential Risks and Considerations

While balance transfer cards can offer a valuable tool for managing debt, it’s crucial to understand the potential risks and considerations before applying. Failing to do so could lead to unexpected consequences and ultimately hinder your debt reduction efforts.

High Interest Rates After Introductory Period

A key risk associated with balance transfer cards is the potential for high interest rates after the introductory period expires. While these cards often offer a 0% APR for a certain period, typically 12 to 18 months, the interest rate can jump significantly once that period ends. If you haven’t paid off the transferred balance by the time the introductory period expires, you’ll start accruing interest at the standard APR, which can be significantly higher than your previous card’s rate.

Missed Payments and Late Fees

Another crucial consideration is the impact of missed payments or late fees. Missing a payment on a balance transfer card can lead to a variety of consequences, including:

- Increased interest rates: Missing payments can trigger a penalty APR, significantly increasing the cost of your debt.

- Late fees: You may be charged a late fee for each missed payment.

- Negative impact on credit score: Late payments can negatively impact your credit score, making it more challenging to secure loans or credit in the future.

Understanding the Terms and Conditions

Before applying for a balance transfer card, carefully review the terms and conditions. Pay close attention to:

- Introductory APR: The duration of the 0% APR period and the standard APR after it ends.

- Balance transfer fees: The percentage or flat fee charged for transferring your balance.

- Annual fees: Whether the card has an annual fee and its amount.

- Late payment fees: The amount of the late fee for missed payments.

- Minimum payment: The minimum amount you must pay each month.

It’s essential to understand the terms and conditions of the balance transfer card to make informed decisions about your debt management strategy.

Ending Remarks

Navigating the world of high balance transfer credit cards requires careful consideration. While they can be a valuable tool for debt management, they’re not a magic bullet. Understanding the terms and conditions, comparing options, and developing a solid repayment plan are crucial to maximizing their benefits and avoiding potential pitfalls. Before taking the plunge, research thoroughly, explore alternatives, and ensure a high balance transfer card aligns with your financial goals and capabilities.

Key Questions Answered

How do I know if a high balance transfer card is right for me?

A high balance transfer card might be suitable if you have high-interest debt you want to consolidate, have good credit, and can commit to a repayment plan to avoid accruing interest after the introductory period.

What are the common eligibility requirements for high balance transfer cards?

Eligibility criteria vary by issuer, but typically include a good credit score (often 670 or higher), sufficient income, and a manageable debt-to-income ratio.

What are the potential risks of using a high balance transfer card?

Risks include high interest rates after the introductory period, missed payments, late fees, and potential for accumulating additional debt if not used responsibly.