Credit cards with transfer offer a unique opportunity to consolidate debt and potentially save money on interest. These cards allow you to move existing balances from other credit cards to a new card with a lower interest rate, effectively lowering your monthly payments and helping you pay off your debt faster.

Understanding the mechanics of credit card transfers, comparing different card offers, and implementing effective strategies are crucial to maximizing the benefits of this financial tool. This guide explores the ins and outs of credit card transfers, empowering you to make informed decisions that align with your financial goals.

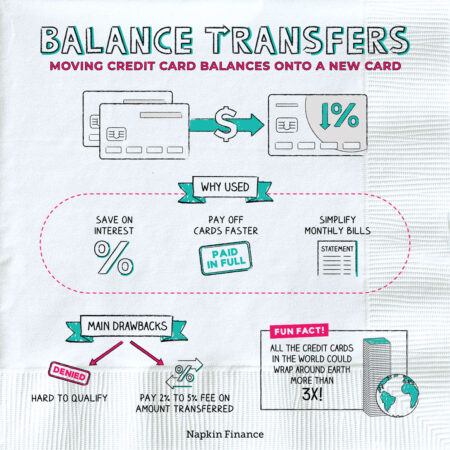

Understanding Credit Card Transfers

Credit card balance transfers allow you to move outstanding balances from one credit card to another. This can be a valuable tool for managing debt, particularly if you’re looking to lower your interest payments.

Benefits of Credit Card Balance Transfers

Balance transfers can offer several advantages, including:

- Lower Interest Rates: Transferring your balance to a card with a lower interest rate can significantly reduce your overall interest charges. This can save you money in the long run, allowing you to pay off your debt faster.

- Debt Consolidation: If you have multiple credit cards with high balances, a balance transfer can help you consolidate your debt into a single account. This simplifies your repayment process and makes it easier to track your progress.

Situations Where a Balance Transfer is Advantageous

A balance transfer can be a beneficial strategy in various situations, including:

- High-Interest Credit Card Debt: If you have a credit card with a high APR, transferring your balance to a card with a lower APR can help you save money on interest charges.

- Multiple Credit Cards: If you have multiple credit cards with balances, consolidating your debt into a single account can simplify your repayment process and potentially lower your overall interest rate.

- Limited Credit History: If you have a limited credit history, a balance transfer can help you build your credit score by demonstrating responsible borrowing behavior. This can make it easier to obtain other forms of credit in the future.

Key Features of Transfer Cards: Credit Cards With Transfer

Balance transfer credit cards can be a valuable tool for consolidating debt and saving money on interest charges. These cards offer a range of features that make them attractive to consumers looking to manage their debt more effectively.

Interest Rates Offered

Interest rates on balance transfer credit cards vary significantly, depending on the issuer and the cardholder’s creditworthiness.

- Introductory Rates: Many balance transfer cards offer a promotional introductory interest rate, typically 0% APR, for a specific period, often 12 to 18 months. These rates can be significantly lower than the standard APRs on other credit cards.

- Standard APRs: After the introductory period ends, the interest rate on a balance transfer card reverts to the standard APR, which can be significantly higher than the introductory rate.

- Variable APRs: Some balance transfer cards have variable APRs, meaning the interest rate can fluctuate based on market conditions.

Transfer Fees

Balance transfer cards typically charge a fee for transferring a balance from another credit card.

- Transfer Fee: The transfer fee is usually a percentage of the amount transferred, ranging from 3% to 5%.

- Introductory Periods: Some cards offer a promotional period where transfer fees are waived.

- Subsequent Rates: After the introductory period, the transfer fee may apply to subsequent balance transfers.

Eligibility Criteria and Credit Score Requirements

To qualify for a balance transfer credit card, applicants must meet certain eligibility criteria, which typically include:

- Good Credit Score: Balance transfer cards generally require a good credit score, typically 670 or higher.

- Income and Debt-to-Income Ratio: Issuers also consider income and debt-to-income ratio to assess an applicant’s ability to repay the transferred balance.

- Credit History: A strong credit history, including on-time payments and responsible credit utilization, is crucial for approval.

Choosing the Right Transfer Card

Selecting the perfect balance transfer card requires careful consideration of your financial needs and the specific features offered by different cards. It’s crucial to compare interest rates, fees, and eligibility criteria to find the best fit for your situation.

Comparing Transfer Card Offers, Credit cards with transfer

A balance transfer card can be a valuable tool for saving money on interest charges, but it’s important to compare different offers to find the best deal. The following table provides a general comparison of some key features:

| Feature | Card A | Card B | Card C |

|---|---|---|---|

| Interest Rate | 0% for 12 months, then 18% APR | 0% for 18 months, then 21% APR | 0% for 24 months, then 24% APR |

| Transfer Fee | 3% of the transferred balance | 2% of the transferred balance | 1% of the transferred balance |

| Eligibility Criteria | Good credit score (700+) | Excellent credit score (750+) | Exceptional credit score (800+) |

Selecting the Best Transfer Card

To choose the most suitable balance transfer card, follow these steps:

- Assess Your Credit Score: Your credit score is a key factor in determining your eligibility for a balance transfer card. Check your credit report and score before applying.

- Compare Interest Rates and Fees: Look for cards with low introductory interest rates and minimal transfer fees.

- Consider the Transfer Period: Choose a card with a transfer period that aligns with your debt repayment plan.

- Evaluate Eligibility Criteria: Ensure you meet the minimum credit score and income requirements for the card.

- Review Other Features: Consider additional benefits such as rewards programs, travel insurance, or purchase protection.

Impact on Credit Utilization

A balance transfer can impact your credit utilization ratio, which is the amount of credit you’re using compared to your available credit.

A high credit utilization ratio can negatively affect your credit score.

When transferring a balance, make sure to account for the new credit limit and adjust your spending accordingly.

Effective Transfer Strategies

Transferring credit card balances can be a smart move to save money on interest charges, but it’s crucial to use the right strategies to maximize your savings and avoid potential pitfalls. This section delves into best practices for transferring balances, designing a plan for managing debt after a transfer, and tips for avoiding common pitfalls.

Maximizing Savings and Minimizing Fees

Balance transfer offers can be a great way to save money on interest charges, but it’s important to understand the associated fees and how they impact your overall savings.

- Compare Transfer Fees: Different credit cards have varying transfer fees, which can range from 0% to 5% of the transferred balance. Always compare these fees before transferring your balance to ensure you’re getting the best deal. For example, a card with a 0% transfer fee and a 3% annual fee might be more advantageous than a card with a 1% transfer fee and a 0% annual fee if you plan to keep the balance for a longer duration.

- Calculate Interest Savings: Compare the interest rate on your current card with the introductory rate offered by the transfer card. Calculate the difference in interest charges you’ll save over the introductory period. Consider using online calculators to determine the potential savings and the time it will take to pay off the balance with the new card. For example, if you have a $5,000 balance on a card with a 18% APR and transfer it to a card with a 0% APR for 12 months, you could save over $900 in interest charges.

- Time Your Transfers: Transfer your balance just before the promotional period on your current card expires. This can help you avoid paying high interest charges during the transition period. For instance, if your current card has a 0% introductory period ending in a month, you should transfer your balance a few days before the expiration date to avoid incurring interest charges.

Managing Debt After a Balance Transfer

Once you’ve transferred your balance, it’s essential to create a plan for managing your debt effectively to ensure you pay it off within the promotional period and avoid accumulating new debt.

- Set a Budget: Develop a realistic budget that allows you to make consistent payments on your transferred balance while covering your essential expenses. This will help you avoid falling behind on your payments and incurring late fees.

- Make More Than the Minimum Payment: While the minimum payment is the least you can pay, it’s crucial to make more than the minimum to pay down your balance faster. This will help you avoid paying interest charges and ultimately save money. For example, if your balance is $5,000 and you have a minimum payment of $50, consider making a payment of $150 or more to accelerate the repayment process.

- Consider Debt Consolidation: If you have multiple credit card balances, debt consolidation could be an option. This involves taking out a loan to pay off all your credit card debts, often with a lower interest rate. However, carefully evaluate the terms of the loan and make sure it fits your financial situation.

Avoiding Common Pitfalls

While balance transfers can be beneficial, it’s important to be aware of potential pitfalls to avoid them and ensure you get the most out of your transfer.

- Transferring Too Much: Transferring more than you can afford to pay off within the promotional period can lead to accumulating high interest charges after the introductory period expires. For example, if you transfer a $10,000 balance with a 0% APR for 12 months and only pay the minimum payment, you’ll still have a significant balance after the introductory period, potentially incurring high interest charges.

- Missing the Transfer Deadline: Make sure you transfer your balance before the promotional period on your current card expires. Otherwise, you may be subject to high interest charges on the remaining balance. For instance, if your current card has a 0% introductory period ending on March 15th, you should transfer your balance before that date to avoid paying interest.

- Ignoring the Terms and Conditions: Carefully read the terms and conditions of the balance transfer offer before accepting it. Pay attention to fees, interest rates, and other conditions that could impact your savings. For example, some cards may have a penalty APR if you miss a payment or make a late payment, which can significantly increase your interest charges.

Alternatives to Credit Card Transfers

While credit card balance transfers can be a helpful tool for managing debt, they are not the only option available. Several alternatives can help you consolidate and pay down your credit card balances more effectively.

Exploring these alternatives allows you to compare their benefits and drawbacks and choose the strategy that best suits your financial situation.

Debt Consolidation Loans

Debt consolidation loans allow you to combine multiple debts, including credit card balances, into a single loan with a lower interest rate. This can save you money on interest payments and simplify your debt management.

Advantages of Debt Consolidation Loans

- Lower Interest Rates: Debt consolidation loans often offer lower interest rates than credit cards, reducing your monthly payments and overall interest charges.

- Simplified Repayment: Instead of juggling multiple credit card payments, you have a single loan payment to manage, making budgeting easier.

- Fixed Interest Rates: Most debt consolidation loans have fixed interest rates, providing predictability and stability in your monthly payments.

Disadvantages of Debt Consolidation Loans

- Potential for Higher Overall Interest: While the interest rate on the loan may be lower than your credit cards, the overall interest paid over the loan’s term could be higher if you take a longer repayment period.

- Credit Score Impact: Applying for a debt consolidation loan can temporarily lower your credit score due to the hard inquiry on your credit report.

- Limited Eligibility: You need good credit to qualify for a debt consolidation loan with favorable terms.

Balance Transfer Services

Balance transfer services allow you to transfer your credit card balances to a new credit card with a lower introductory APR. This can help you save money on interest charges during the introductory period.

Advantages of Balance Transfer Services

- Lower Introductory APR: Balance transfer offers typically come with a 0% or low introductory APR for a limited period, allowing you to focus on paying down the principal.

- No Transfer Fees (Sometimes): Some balance transfer offers waive transfer fees, saving you money on upfront costs.

Disadvantages of Balance Transfer Services

- Limited Time Period: The introductory APR usually lasts for a set period, after which the interest rate may increase significantly.

- Potential for Higher Interest Rates: If you don’t pay off the balance before the introductory period ends, you’ll be subject to the higher regular APR.

- Credit Score Impact: Applying for a new credit card for a balance transfer can affect your credit score.

Choosing the Right Debt Management Strategy

The best debt management strategy depends on your individual circumstances, including:

- Amount of Debt: If you have a significant amount of debt, a debt consolidation loan or balance transfer service might be more beneficial.

- Credit Score: A good credit score increases your chances of qualifying for lower interest rates and favorable terms.

- Financial Goals: Consider your financial goals and how long you’re willing to spend paying off your debt.

It’s crucial to compare offers and terms from multiple lenders before making a decision. You should also carefully consider the potential impact on your credit score and the long-term costs associated with each option.

Closing Summary

By carefully analyzing your options, choosing the right credit card transfer, and implementing effective strategies, you can leverage the power of credit card transfers to manage your debt more efficiently and achieve financial freedom. Remember to consider the transfer period, credit utilization, and potential fees associated with each card. With careful planning and a proactive approach, credit card transfers can become a valuable tool in your financial journey.

Helpful Answers

What is the minimum credit score required for a balance transfer card?

Credit score requirements vary depending on the card issuer, but generally, a good credit score (at least 670) is needed to qualify for a balance transfer card with favorable terms.

How long does it take for a balance transfer to be processed?

The processing time for a balance transfer can range from a few days to several weeks, depending on the card issuer and the complexity of the transfer.

What are the risks associated with credit card balance transfers?

Potential risks include high transfer fees, limited introductory periods, and the possibility of accruing additional debt if you don’t pay down the transferred balance within the promotional period.

Can I transfer a balance from a store credit card to a regular credit card?

While it’s possible, store credit cards often have higher interest rates and stricter transfer policies. It’s advisable to check with the card issuer to confirm if transfers are allowed.