Credit card with balance transfer can be a lifesaver when you’re drowning in high-interest debt. It’s like a financial reset button, allowing you to consolidate your existing balances onto a new card with a lower interest rate. Imagine the relief of finally getting ahead of those crippling payments! But before you dive into this debt-busting strategy, it’s essential to understand the intricacies of balance transfer cards and how to choose the right one for your needs.

These cards offer a tempting introductory period with 0% APR, giving you breathing room to pay down your debt without accumulating interest. However, it’s crucial to be aware of potential pitfalls like balance transfer fees, minimum payments, and the consequences of not paying off the balance before the introductory period ends. Understanding these factors will help you navigate the world of balance transfer cards and make informed decisions that benefit your financial well-being.

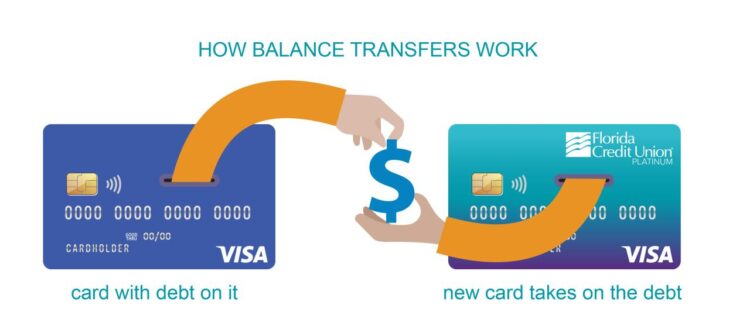

What is a Balance Transfer Credit Card?

A balance transfer credit card is a type of credit card that allows you to transfer outstanding balances from other credit cards to it. This can be beneficial if you have high-interest credit card debt, as you may be able to secure a lower interest rate on the balance transfer card.

A balance transfer credit card works by allowing you to move the balance from your existing credit card to the new card. This new card usually has a lower interest rate, which can save you money on interest charges over time.

Situations Where a Balance Transfer Credit Card Can Be Beneficial

Balance transfer credit cards can be particularly useful in situations where you have high-interest credit card debt. For example, if you have a credit card with an interest rate of 20% and you can find a balance transfer card with an interest rate of 5%, you could save a significant amount of money on interest charges.

Balance transfer cards can also be helpful if you are struggling to make your minimum payments on your existing credit cards. By transferring your balance to a card with a lower interest rate, you may be able to reduce your monthly payments and free up some cash flow.

Advantages and Disadvantages of Using a Balance Transfer Credit Card

There are several advantages and disadvantages to using a balance transfer credit card.

Advantages

- Lower interest rates: Balance transfer cards typically offer lower interest rates than other types of credit cards. This can help you save money on interest charges over time.

- Consolidation of debt: A balance transfer card can help you consolidate your debt into one manageable payment. This can make it easier to track your payments and avoid late fees.

- 0% introductory APR: Many balance transfer cards offer a 0% introductory APR for a certain period of time. This can give you a chance to pay down your debt without incurring any interest charges.

Disadvantages

- Balance transfer fees: Most balance transfer cards charge a fee for transferring your balance. This fee is typically a percentage of the amount transferred, so it can be substantial if you have a large balance.

- Limited time offer: The 0% introductory APR on a balance transfer card is usually only valid for a limited time. After the introductory period expires, the interest rate will revert to the standard APR, which can be quite high.

- Potential for overspending: If you are not careful, it is easy to overspend on a balance transfer card. This can lead to even more debt than you had before.

Key Features of Balance Transfer Credit Cards

Balance transfer credit cards offer a compelling solution for individuals looking to consolidate high-interest debt and potentially save money on interest charges. These cards often come with enticing introductory periods of 0% APR, allowing you to transfer your existing balances without accruing interest for a specified duration. However, understanding the key features of these cards is crucial to making informed decisions.

Introductory Period (0% APR)

The most attractive feature of balance transfer credit cards is the introductory period with 0% APR. This period typically lasts for a set duration, ranging from 6 to 18 months, during which you won’t incur any interest charges on the transferred balance. This grace period allows you to focus on paying down the principal balance without the added burden of interest accumulation.

Balance Transfer Fees

While balance transfer credit cards offer the advantage of 0% APR, they often come with a balance transfer fee. This fee is usually a percentage of the transferred balance, ranging from 3% to 5%. It’s important to consider this fee when evaluating the overall cost savings of a balance transfer.

Minimum Payments

Balance transfer credit cards typically have minimum payment requirements, which are a fixed percentage of the outstanding balance or a set dollar amount, whichever is higher. It’s essential to make at least the minimum payment each month to avoid late fees and maintain a good credit score.

Credit Limit, Credit card with balance transfer

The credit limit on a balance transfer credit card determines the maximum amount of debt you can transfer. It’s crucial to choose a card with a credit limit that comfortably accommodates your existing balances.

Other Fees

In addition to balance transfer fees, balance transfer credit cards may charge other fees, such as:

- Annual Fee: Some cards have an annual fee, which can range from $0 to $100 or more.

- Late Payment Fee: If you miss a payment deadline, you may be charged a late payment fee, typically around $25 to $35.

- Over-the-Limit Fee: If you exceed your credit limit, you may be charged an over-the-limit fee.

- Foreign Transaction Fee: Some cards charge a foreign transaction fee for purchases made outside of the United States.

Comparison of Balance Transfer Credit Cards

The features and fees of balance transfer credit cards can vary significantly from issuer to issuer. Here’s a comparison of key features for three popular balance transfer credit cards:

| Card | Introductory APR | Balance Transfer Fee | Annual Fee | Other Fees |

|---|---|---|---|---|

| Chase Slate | 0% APR for 15 months | 5% of the amount transferred (minimum $5) | $0 | Late Payment Fee: $39; Over-the-Limit Fee: $39 |

| Citi Simplicity® Card | 0% APR for 21 months | 3% of the amount transferred (minimum $5) | $0 | Late Payment Fee: $25; Over-the-Limit Fee: $25 |

| Discover it® Balance Transfer | 0% APR for 18 months | 3% of the amount transferred (minimum $5) | $0 | Late Payment Fee: $29; Over-the-Limit Fee: $29 |

How to Choose the Right Balance Transfer Credit Card

Choosing the right balance transfer credit card is crucial to effectively manage your debt and potentially save money on interest charges. By carefully considering your individual needs and circumstances, you can find a card that aligns with your financial goals.

Factors to Consider When Choosing a Balance Transfer Credit Card

The decision-making process for selecting a balance transfer credit card involves evaluating several factors, including:

- Existing Credit Card Debt Amount: The amount of debt you currently have on your existing credit cards is a key factor in determining the right balance transfer credit card. You’ll want to choose a card with a credit limit that is sufficient to cover your existing debt, allowing you to transfer the entire balance.

- Credit Score: Your credit score plays a significant role in the approval process and the interest rates you qualify for. A higher credit score typically leads to more favorable terms, including lower interest rates and potentially higher credit limits.

- Interest Rate: The interest rate on a balance transfer credit card is a crucial factor. A lower interest rate can result in significant savings on interest charges over time. Aim for a card with a low introductory APR (Annual Percentage Rate) for balance transfers, often lasting for a specific period, such as 12 to 18 months.

- Balance Transfer Fees: Balance transfer fees are charged when you transfer a balance from another credit card. These fees can vary depending on the card issuer and the amount transferred. Some cards offer a 0% balance transfer fee for a limited time, while others charge a percentage of the transferred balance.

- Other Card Benefits: Consider other card benefits, such as rewards programs, travel insurance, purchase protection, and fraud protection. These benefits can add value to your credit card and enhance your overall experience.

Examples of Scenarios and Corresponding Recommendations

To illustrate the process of choosing the right balance transfer credit card, consider these scenarios and recommendations:

- Scenario 1: High Debt, Good Credit Score: If you have a significant amount of credit card debt and a good credit score, you might be eligible for a balance transfer card with a low introductory APR and a high credit limit. Look for a card with a 0% introductory APR for 12 to 18 months, allowing you to focus on paying down your debt without accumulating interest.

- Scenario 2: Average Debt, Average Credit Score: If you have a moderate amount of debt and an average credit score, you might consider a balance transfer card with a slightly higher introductory APR but a lower balance transfer fee. This can help you manage your debt effectively while minimizing upfront costs.

- Scenario 3: Low Debt, Poor Credit Score: If you have a small amount of debt and a poor credit score, you might have limited options for balance transfer cards. Consider contacting a credit counseling agency or exploring secured credit cards to improve your credit score before applying for a balance transfer card.

The Process of Transferring a Balance

Transferring a balance from one credit card to another involves a series of steps, from applying for a balance transfer credit card to initiating the transfer and monitoring the progress. The process is typically straightforward, but there are potential challenges to be aware of.

Applying for a Balance Transfer Credit Card

Before transferring your balance, you need to apply for a balance transfer credit card.

This involves submitting a credit card application to a lender and providing your personal and financial information.

The lender will review your application and determine if you qualify for the card based on your credit score, income, and other factors.

- Gather the necessary information, including your Social Security number, income, and employment history.

- Fill out the application form online or by mail, providing accurate information.

- Review the terms and conditions carefully, including the interest rate, balance transfer fee, and introductory period.

- Once you submit your application, the lender will review it and notify you of their decision.

- If approved, you will receive a credit card and a balance transfer request form.

Initiating the Balance Transfer

Once you have received your balance transfer credit card, you can initiate the transfer by following the instructions provided by the lender.

- Obtain the account number and balance of the credit card you want to transfer.

- Complete the balance transfer request form provided by your new credit card issuer.

- Submit the form to the lender, either online, by mail, or by phone.

- The lender will process the request and transfer the balance to your new credit card.

- It typically takes a few business days for the balance transfer to be completed.

Potential Challenges During the Balance Transfer Process

While the balance transfer process is generally straightforward, there are some potential challenges you might encounter.

- Credit card approval: Not everyone is approved for a balance transfer credit card.

If you have a low credit score or a history of missed payments, you may be denied. - Balance transfer fees: Many balance transfer credit cards charge a fee, typically a percentage of the balance transferred.

It’s important to factor in these fees when comparing offers. - Introductory periods: Balance transfer credit cards often offer an introductory period with a 0% APR.

However, this period is usually limited, and the interest rate will increase after it expires. - Transfer limits: Credit card issuers may have limits on the amount of money you can transfer.

This could affect your ability to transfer your entire balance. - Transfer delays: It can take several days for a balance transfer to be completed.

This could result in interest charges on your original credit card if you do not pay the balance before the transfer is finalized.

Managing Your Balance Transfer Credit Card

A balance transfer credit card can be a valuable tool for saving money on interest charges and paying off debt faster, but only if you manage it wisely. Here are some essential strategies to ensure you make the most of your balance transfer card and avoid falling into further debt.

Paying More Than the Minimum Payment

Making only the minimum payment on your balance transfer credit card will take you years to pay off your debt and cost you significantly in interest charges. It’s crucial to pay more than the minimum payment each month to accelerate your debt reduction and minimize interest accumulation. Paying more than the minimum payment is vital for effectively managing a balance transfer credit card. Here’s why:

- Reduced Interest Charges: By paying more than the minimum, you reduce the outstanding balance, which in turn reduces the amount of interest you accrue.

- Faster Debt Repayment: Paying extra towards your balance will significantly shorten the time it takes to pay off your debt. This can save you thousands of dollars in interest over the long run.

- Improved Credit Score: Making consistent payments above the minimum amount demonstrates responsible credit management and positively impacts your credit score.

Consequences of Not Paying the Balance Before the Introductory Period Ends

The introductory period for a balance transfer credit card is typically 12-18 months, during which you enjoy a low or 0% APR. However, if you don’t pay off the transferred balance before the introductory period ends, the regular APR will kick in, often at a much higher rate. This can quickly increase your debt and make it difficult to manage. Here are some potential consequences:

- Higher Interest Rates: When the introductory period ends, the regular APR applies, leading to significantly higher interest charges and making it more challenging to pay off your debt.

- Increased Monthly Payments: As interest accrues, your monthly payments may increase, putting a strain on your budget and making it harder to manage your finances.

- Negative Impact on Credit Score: Failing to make payments on time can negatively impact your credit score, making it harder to obtain loans or credit cards in the future.

Avoiding Future Credit Card Debt

While a balance transfer card can help you manage existing debt, it’s crucial to avoid accumulating new credit card debt. Here are some tips to prevent future debt:

- Track Your Spending: Monitor your spending carefully to identify areas where you can cut back and avoid unnecessary purchases.

- Set a Budget: Create a realistic budget that accounts for your income and expenses, ensuring you have enough money to cover your needs and avoid relying on credit cards.

- Use Cash: Pay for purchases with cash whenever possible, as it can help you stay within your budget and avoid the temptation to overspend.

- Avoid Impulse Purchases: Before making a purchase, take time to consider if it’s truly necessary and if you can afford it.

Alternatives to Balance Transfer Credit Cards

While balance transfer credit cards offer a tempting solution for managing credit card debt, they aren’t the only option available. Exploring alternative methods can help you find the best strategy for your specific financial situation.

Debt Consolidation Loans

Debt consolidation loans allow you to combine multiple debts into a single loan with a lower interest rate. This can simplify your monthly payments and potentially save you money on interest.

- Advantages:

- Lower interest rates can reduce your overall debt cost.

- Simplified payments with a single monthly payment.

- Potential for a longer repayment term, making payments more manageable.

- Disadvantages:

- You may need good credit to qualify for a low interest rate.

- Consolidation can extend your repayment period, increasing the total interest paid.

- If you don’t improve your spending habits, you could accumulate more debt.

Debt Management Programs

Debt management programs (DMPs) are offered by non-profit credit counseling agencies. These programs work with creditors to lower interest rates, reduce monthly payments, and create a structured repayment plan.

- Advantages:

- Lower monthly payments can improve your cash flow.

- Creditors may reduce interest rates and fees.

- DMPs provide support and guidance in managing your debt.

- Disadvantages:

- DMPs typically involve a monthly fee.

- Your credit score may be negatively impacted during the program.

- You may need to close existing credit cards.

Balance Transfer Checks

Some credit card issuers offer balance transfer checks, which allow you to transfer balances from other credit cards directly to your account. This can be a convenient option if you have multiple debts to consolidate.

- Advantages:

- Easy way to transfer balances from multiple cards.

- Can potentially save on interest charges.

- Disadvantages:

- May have a higher balance transfer fee than traditional balance transfers.

- Limited availability from some issuers.

Personal Loans

Personal loans are unsecured loans that can be used for a variety of purposes, including debt consolidation. They often offer lower interest rates than credit cards.

- Advantages:

- Lower interest rates than credit cards.

- Fixed monthly payments, making budgeting easier.

- Faster approval and funding compared to some other options.

- Disadvantages:

- You may need good credit to qualify for a low interest rate.

- Higher interest rates than some other debt consolidation options.

Considerations for Using a Balance Transfer Credit Card

While balance transfer credit cards can be a valuable tool for saving money on interest, it’s crucial to understand the potential risks and use them responsibly. Failing to do so could lead to a situation where you end up paying more than you originally owed.

Potential Risks of Balance Transfer Credit Cards

Understanding the potential risks associated with balance transfer credit cards is essential before applying for one. These risks can significantly impact your financial well-being if not managed carefully.

- High Balance Transfer Fees: Many balance transfer credit cards charge a fee for transferring your balance, typically a percentage of the amount transferred. These fees can add up, especially if you’re transferring a large balance.

- Introductory APR Period Expiration: The biggest advantage of a balance transfer credit card is the introductory 0% APR period. However, this period is usually temporary, and once it expires, the interest rate can jump significantly. If you haven’t paid off the balance by then, you’ll start accruing interest at a much higher rate, potentially eroding any savings you initially gained.

- Late Payment Penalties: Missing a payment on your balance transfer credit card can result in late payment fees, which can quickly add up. Additionally, late payments can negatively impact your credit score.

- Impact on Credit Score: Applying for a new credit card can temporarily lower your credit score, especially if you have several recent inquiries. This is because credit card applications involve a hard inquiry, which is a check on your credit history.

Using a Balance Transfer Credit Card Responsibly

To avoid the potential risks and maximize the benefits of a balance transfer credit card, consider these responsible practices:

- Pay off the balance before the introductory period ends: The most important step is to ensure you pay off the balance before the introductory 0% APR period expires. Failing to do so will result in a significant increase in interest charges, negating any savings you initially achieved.

- Avoid incurring new debt on the balance transfer card: Resist the temptation to use the balance transfer credit card for new purchases. The goal is to pay off the transferred balance, not accumulate more debt. Focus on paying down the existing debt and avoid adding new charges.

- Monitor your credit score and utilization: Keep track of your credit score and utilization rate. A high utilization rate (the amount of credit you’re using compared to your total available credit) can negatively impact your credit score. Strive to keep your utilization below 30%.

- Set a budget and stick to it: Create a budget that includes your minimum monthly payment on the balance transfer credit card. This will help you stay on track and ensure you have enough funds to make timely payments.

Potential Pitfalls of Balance Transfer Credit Cards

Despite their potential benefits, balance transfer credit cards can pose significant pitfalls if not used cautiously. These pitfalls can lead to financial hardship if not addressed proactively.

- Not paying off the balance before the introductory period ends: This is arguably the most common pitfall associated with balance transfer credit cards. Once the introductory period expires, the interest rate on the remaining balance can skyrocket, potentially leading to significant interest charges.

- Incurring new debt on the balance transfer card: Using the balance transfer credit card for new purchases defeats the purpose of transferring your balance to a lower interest rate. This can quickly lead to a snowball effect of debt, making it difficult to pay off the balance.

- Neglecting to monitor credit score and utilization: Failing to monitor your credit score and utilization rate can lead to negative consequences. A low credit score can make it harder to qualify for future loans or credit cards, while a high utilization rate can further impact your credit score.

Conclusion: Credit Card With Balance Transfer

Choosing a credit card with balance transfer can be a strategic move to conquer your debt, but it’s not a magic solution. Remember to do your research, choose wisely, and manage your finances responsibly. By understanding the nuances of balance transfer cards, you can harness their potential to take control of your debt and embark on a path towards financial freedom.

Answers to Common Questions

What is the minimum credit score required for a balance transfer card?

The minimum credit score required varies depending on the issuer and card. Generally, you’ll need a good credit score (at least 670) to qualify for a balance transfer card with a low interest rate.

How long does it take for a balance transfer to be processed?

The processing time for a balance transfer can range from a few days to several weeks. It depends on the card issuer and the complexity of the transfer.

Can I transfer my balance to a different card from the same issuer?

Yes, you can often transfer your balance to a different card from the same issuer, but you might need to meet certain eligibility requirements.

Can I transfer my balance from a store credit card?

Some balance transfer cards allow you to transfer balances from store credit cards, but this isn’t always possible. It’s best to check with the card issuer to confirm.

What happens if I don’t pay off my balance before the introductory period ends?

If you don’t pay off your balance before the introductory period ends, the interest rate will revert to the standard APR, which is typically much higher. This can quickly lead to a significant increase in your debt.