Best balance transfer cards for excellent credit offer a powerful way to save money on existing debt. These cards, specifically designed for individuals with strong credit scores, provide the opportunity to transfer high-interest balances to a new card with a lower introductory APR. This can lead to significant savings on interest charges, making it easier to pay down debt and improve your financial well-being.

The benefits of balance transfer cards for excellent credit go beyond just low interest rates. Many cards also offer rewards programs, travel perks, or cash back offers, allowing you to earn additional value while you pay down your debt. But with so many options available, it’s important to carefully consider factors like transfer fees, introductory periods, and ongoing APRs to find the best card for your needs.

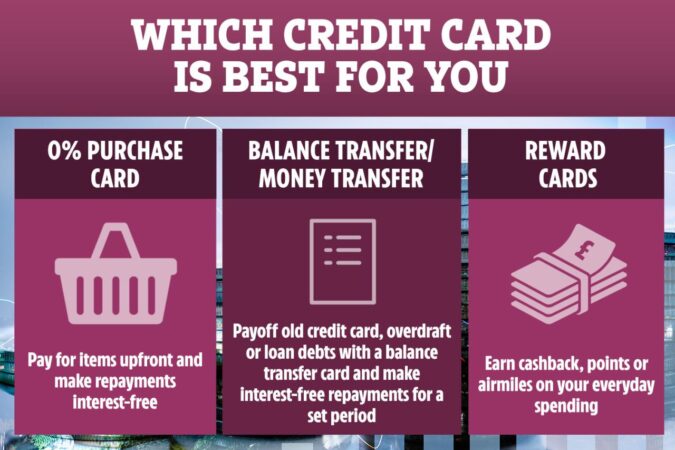

Introduction to Balance Transfer Cards

Balance transfer cards are credit cards designed to help consumers consolidate high-interest debt from other credit cards by transferring the balance to a new card with a lower interest rate. This can save you money on interest charges and help you pay off your debt faster.

Balance transfer cards are particularly beneficial for individuals with excellent credit, as they often qualify for the most favorable terms, such as low introductory APRs and generous balance transfer limits.

Factors to Consider When Choosing a Balance Transfer Card

Choosing the right balance transfer card requires careful consideration of several factors. Here are some key elements to keep in mind:

Interest Rates

The most important factor is the interest rate, as it directly impacts the amount of interest you’ll pay over time. Look for cards with low introductory APRs, typically offered for a specific period (e.g., 12-18 months). After the introductory period, the interest rate will revert to the card’s standard APR, so make sure you can pay off the transferred balance before the promotional period ends.

Transfer Fees

Balance transfer cards often charge a fee for transferring your balance. These fees can range from 3% to 5% of the transferred amount. Carefully compare the transfer fees across different cards and factor them into your calculations to determine the overall cost.

Introductory Periods

The length of the introductory period is crucial. A longer introductory period gives you more time to pay off the balance at the lower interest rate. Aim for cards with introductory periods of at least 12 months, ideally 18 months or longer.

Benefits of Balance Transfer Cards for Excellent Credit

Individuals with excellent credit scores often have access to a wider range of financial products and services, including balance transfer cards. These cards can offer significant advantages, especially when it comes to managing existing debt.

Balance transfer cards allow you to move outstanding balances from other credit cards to a new card with a lower introductory APR (Annual Percentage Rate). This can save you a substantial amount of money in interest charges over time, especially if you have a large balance and a high interest rate on your existing card.

Lower Introductory APRs

Lower introductory APRs are a primary benefit of balance transfer cards for individuals with excellent credit. These promotional rates typically last for a limited period, such as 12 to 18 months, and can significantly reduce the cost of carrying a balance. For example, if you have a $10,000 balance on a credit card with a 20% APR and transfer it to a balance transfer card with a 0% introductory APR for 18 months, you’ll save thousands of dollars in interest charges during that period.

Rewards Programs

Many balance transfer cards offer rewards programs, such as cash back, travel miles, or points, that can offset the cost of transferring your balance. These rewards can be redeemed for a variety of benefits, including merchandise, gift cards, travel expenses, or statement credits.

Travel Perks

Some balance transfer cards offer travel perks, such as airport lounge access, travel insurance, or priority boarding. These benefits can be particularly valuable for frequent travelers who value convenience and peace of mind.

Cash Back Offers

Some balance transfer cards offer cash back rewards on purchases, which can be a valuable perk for individuals who use their cards frequently. Cash back rewards can be redeemed for statement credits or deposited into a bank account.

Factors to Consider When Choosing a Balance Transfer Card

Choosing the right balance transfer card can save you significant money on interest charges. However, not all cards are created equal, and certain factors play a crucial role in determining the best fit for your financial needs.

Interest Rates

Interest rates are a primary consideration when comparing balance transfer cards. A lower interest rate translates to lower interest charges, ultimately saving you money.

- Introductory APR: This is the initial interest rate offered for a specified period. It’s typically a low rate, often 0%, which helps you pay down your balance quickly.

- Standard APR: This is the interest rate applied after the introductory period ends. It’s usually higher than the introductory APR.

It’s important to compare the introductory and standard APRs across different cards to determine the overall cost savings.

Transfer Fees

Balance transfer cards often charge a fee for transferring your balance from another card. This fee can vary depending on the card issuer and the amount transferred.

- Percentage Fee: This fee is calculated as a percentage of the balance transferred.

- Flat Fee: This fee is a fixed amount, regardless of the balance transferred.

Transfer fees can significantly impact the overall cost savings of a balance transfer.

Introductory Period

The introductory period is the duration for which the low introductory APR applies. It’s crucial to choose a card with a long enough introductory period to give you ample time to pay down your balance.

- Length of Introductory Period: The introductory period can range from a few months to a year or more.

A longer introductory period allows you to make significant progress in paying down your debt before the higher standard APR kicks in.

Key Features of Popular Balance Transfer Cards

The following table compares the key features of some popular balance transfer cards, including interest rates, transfer fees, introductory periods, and rewards programs:

| Card Name | Introductory APR | Standard APR | Transfer Fee | Introductory Period | Rewards Program |

|---|---|---|---|---|---|

| Card A | 0% | 18.99% | 3% of balance transferred | 18 months | Cash back |

| Card B | 0% | 16.99% | $5 | 15 months | Travel miles |

| Card C | 0% | 19.99% | 2% of balance transferred | 12 months | Points redeemable for merchandise |

How to Apply for a Balance Transfer Card

Applying for a balance transfer card is similar to applying for any other credit card. However, you may need to provide additional information, such as the account number and balance of the debt you want to transfer.

Steps Involved in Applying for a Balance Transfer Card

The application process for a balance transfer card typically involves these steps:

- Choose a balance transfer card: Research different balance transfer cards and compare their features, such as introductory APR, balance transfer fees, and credit score requirements.

- Check your credit score: Before applying, it’s wise to check your credit score to ensure you meet the eligibility criteria. You can get a free credit score from websites like Credit Karma or Experian.

- Gather the necessary information: You’ll need your Social Security number, income, and employment information. You may also need to provide the account number and balance of the debt you want to transfer.

- Complete the application: You can apply online, by phone, or in person. The application process usually involves filling out a form with your personal and financial information.

- Wait for a decision: The lender will review your application and make a decision. You may receive a response within a few days.

- Transfer your balance: Once approved, you can transfer your balance from your existing credit card to the new balance transfer card. This usually involves providing the new card issuer with the account number and balance of the debt you want to transfer.

Required Documentation and Information

The specific documentation and information you’ll need to provide will vary depending on the lender. However, you can expect to provide the following:

- Personal information: This includes your name, address, Social Security number, date of birth, and contact information.

- Income and employment information: This may include your income, employment history, and pay stubs.

- Credit card information: This includes the account number and balance of the debt you want to transfer.

- Financial information: This may include your bank account information and other credit card accounts.

Credit Score Requirements and Eligibility Criteria

Balance transfer cards are typically designed for consumers with excellent credit. This means you’ll need a credit score of at least 700 to qualify for the best offers. However, some lenders may offer balance transfer cards to consumers with lower credit scores.

The credit score requirements and eligibility criteria for balance transfer cards vary depending on the lender.

Tips for Using Balance Transfer Cards Effectively

Balance transfer cards can be a powerful tool for saving money on interest charges, but only if used strategically. Understanding the nuances of balance transfer cards and employing effective strategies is crucial for maximizing their benefits.

Maximizing Benefits

Maximizing the benefits of a balance transfer card involves understanding the mechanics of the introductory period and employing strategies to avoid incurring additional interest charges.

- Transfer Your Entire Balance: Transferring your entire balance from your existing high-interest card to your balance transfer card is the first step to maximizing savings. This ensures that you benefit from the lower introductory APR on the entire balance.

- Avoid New Purchases: Resist the temptation to make new purchases on your balance transfer card during the introductory period. Any new purchases will accrue interest at the card’s regular APR, negating the benefits of the balance transfer.

- Pay More Than the Minimum: While you’ll enjoy a lower APR during the introductory period, make sure to pay more than the minimum amount due each month. This will help you pay down the balance faster and avoid accruing interest once the introductory period ends.

Avoiding Additional Interest Charges

One of the key benefits of balance transfer cards is the introductory period with a lower APR. However, it’s crucial to avoid actions that could trigger interest charges during this period.

- Avoid Late Payments: Late payments can trigger interest charges even during the introductory period. Ensure you make your payments on time to maintain the benefit of the low APR.

- Pay Attention to Fees: Some balance transfer cards charge a balance transfer fee, typically a percentage of the transferred amount. Factor these fees into your calculations to ensure the balance transfer is truly beneficial.

- Understand Grace Periods: Some cards offer a grace period for new purchases, but this may not apply to balance transfers. Be aware of the grace period policies to avoid accruing interest on the transferred balance.

Paying Down the Balance Before the Introductory Period Ends

The introductory period for a balance transfer card is usually temporary, lasting for a specific period (often 12-18 months). Failing to pay down the balance before the introductory period ends can result in a significant increase in interest charges.

- Set a Payment Schedule: Develop a realistic payment schedule that allows you to pay down the balance before the introductory period ends. Consider using online budgeting tools or apps to help you track your progress.

- Consider a Debt Consolidation Loan: If you find it challenging to pay down the balance within the introductory period, consider a debt consolidation loan. A consolidation loan can help you consolidate multiple debts into one with a lower interest rate, making it easier to manage your debt.

- Seek Professional Help: If you’re struggling to manage your debt, don’t hesitate to seek professional help from a credit counselor or financial advisor. They can provide guidance and support to help you create a plan to pay down your debt effectively.

Managing Credit Card Debt Responsibly

Using balance transfer cards effectively is one step towards managing credit card debt responsibly.

- Avoid Overspending: Overspending is a major contributor to credit card debt. Track your spending and develop a budget that allows you to live within your means and avoid accumulating excessive debt.

- Pay Your Bills on Time: Making timely payments is crucial for maintaining a good credit score and avoiding late fees. Set reminders or use automatic payments to ensure you never miss a payment deadline.

- Limit the Number of Credit Cards: Having too many credit cards can increase your chances of overspending and make it harder to manage your debt. Focus on using one or two cards responsibly and avoid applying for new cards unless absolutely necessary.

Alternatives to Balance Transfer Cards: Best Balance Transfer Cards For Excellent Credit

While balance transfer cards are a popular option for debt consolidation, they aren’t the only solution. Several alternatives offer unique benefits and drawbacks, making it essential to compare them carefully to determine the best fit for your financial situation.

Personal Loans

Personal loans are a type of unsecured loan that can be used for various purposes, including debt consolidation. They offer a fixed interest rate and a set repayment term, making it easier to budget for monthly payments.

Advantages of Personal Loans

- Lower Interest Rates: Personal loans often have lower interest rates than credit cards, especially if you have excellent credit. This can save you money on interest charges over time.

- Fixed Monthly Payments: With a fixed interest rate and repayment term, you know exactly how much you’ll need to pay each month, making budgeting easier.

- Faster Debt Consolidation: Personal loans can be used to pay off multiple debts quickly, potentially saving you time and interest charges.

Disadvantages of Personal Loans

- Origination Fees: Some lenders charge origination fees, which are a percentage of the loan amount. This can add to the overall cost of the loan.

- Credit Score Impact: Applying for a personal loan can impact your credit score, especially if you apply for multiple loans simultaneously.

- Limited Flexibility: Once you take out a personal loan, you’re locked into a specific repayment term, which may not be ideal if your financial situation changes.

Debt Consolidation Loans, Best balance transfer cards for excellent credit

Debt consolidation loans are a type of personal loan specifically designed to pay off multiple debts, such as credit cards, medical bills, or personal loans. These loans typically have lower interest rates than credit cards, making them an attractive option for debt consolidation.

Advantages of Debt Consolidation Loans

- Simplified Payments: Instead of making multiple payments to different creditors, you’ll only have one monthly payment to the debt consolidation loan lender.

- Lower Interest Rates: Debt consolidation loans often have lower interest rates than credit cards, saving you money on interest charges over time.

- Potential for Credit Score Improvement: Consolidating your debt can help improve your credit score by reducing your credit utilization ratio.

Disadvantages of Debt Consolidation Loans

- Longer Repayment Terms: Debt consolidation loans can have longer repayment terms than credit cards, potentially leading to higher overall interest charges.

- Potential for Overspending: If you don’t manage your finances carefully, you could end up accumulating more debt after consolidating your existing debt.

- Credit Score Impact: Applying for a debt consolidation loan can impact your credit score, especially if you apply for multiple loans simultaneously.

Conclusive Thoughts

By understanding the ins and outs of balance transfer cards and choosing the right card for your situation, you can leverage the power of these financial tools to save money, reduce debt, and improve your credit score. Whether you’re looking to consolidate debt, take advantage of a low introductory APR, or earn valuable rewards, a balance transfer card can be a valuable addition to your financial arsenal.

Questions and Answers

How long do introductory APRs typically last on balance transfer cards?

Introductory APRs on balance transfer cards typically last for 12 to 18 months, but some cards may offer longer periods. It’s essential to carefully review the terms and conditions of each card to determine the specific introductory period and any applicable fees.

What happens after the introductory period ends on a balance transfer card?

Once the introductory period ends, the balance transfer card will revert to its standard APR, which is often significantly higher than the introductory rate. To avoid accruing substantial interest charges, it’s crucial to pay down the balance before the introductory period expires.

Are there any income requirements for balance transfer cards?

While specific income requirements may vary depending on the issuer and the card, balance transfer cards generally don’t have strict income requirements. The primary focus is on creditworthiness and credit score.